What words or phrases come to mind when you think about target date funds? “Set it and forget it”, low maintenance, ease of use, and instant diversification come to mind. While a lot of articles mention these as benefits, this article is going to look at some of the downsides and why you should NOT consider target date funds for your retirement. Before we dive into the negatives, let’s look at how traditional target date funds work and the pros and cons.

How a target date fund works

Basically, a target date fund allocates itself as you work toward retirement age. I’m not going to go into the history of target date funds so all you need to know is that in the early life stages of the fund, the majority of the portfolio is going to be allocated to equities (also called stocks) while the rest will be allocated to bonds. As the fund approaches its target date (which is why they’re called that way in the first place), it will progressively shift toward bonds so by the time you retire, the majority of the portfolio will be allocated toward bonds instead of equities. These allocations are all done by the manager and no input is required from the user besides periodically depositing funds into the account to grow their retirement account. While this may sound great, continue reading to discover the pros and cons of a target date fund.

Pros

Ease of use – target date funds are meant to be easy to use. A user of a target date fund would simply purchase a fund with the year they want to retire in using a brokerage account and would periodically continue to deposit funds in their retirement account. No input is required from the user so target date funds are seen as “set it and forget it”-type funds.

Low maintenance – from the user perspective, there is low maintenance required because the manager does all the work of allocating the portfolio every year. Thus, a target date fund does not require constant monitoring from the user like a traditional investment account.

Instant diversification – target date funds are typically a blend of stocks and bonds and provide immediate diversification which lowers risk. This is great for those who are looking for safe investments, although we will debate about the true safety of target date funds below.

Cons

One size fits all – target date funds assume that one type of fund fits everyone’s goals. However this may not be the case depending on your goals for retirement and how much you need to comfortably retire. A target date fund critically misses the feature of customization and assumes that it will satisfy everyone’s needs.

Higher expense ratios – in some target date funds, there are additional fees for the underlying mutual funds and management fees. Be sure to read the prospectus regarding fees when you are considering target date funds or any investment.

Low returns – while there are many different target date funds to choose from and they all have different returns, studies have shown that target date funds actually underperform a balanced portfolio! This will be the main focus of the article on why you should think twice before purchasing a target date fund and we’ll go into details below.

Questionable safety – one could argue that a balanced portfolio is actually safer than a traditional target date fund because it always remains constant and disregards the timing of the market while a target date fund is always shifting. For example, if interest rates are low (like in the present environment) and a target date fund starts shifting to bonds since you’re close to retirement, you would be essentially buying bonds for a premium while receiving low yields! Remember that bond yields and price are inverse of each other so when one goes up, the other goes down. Thus, for true safety a balanced portfolio would have lower risk while delivering higher returns! Continue reading below to find out more.

Fatal Flaw of Target Date Funds – Poor Performance with Questionable Risk

The disadvantages mentioned above may be worth it if target date funds actually performed in line with the market. Unfortunately, they don’t. A study conducted by Rob Arnott and his team at Research Affiliates, a leader in smart beta and asset allocation, discovered that a balanced portfolio split 50-50 between stocks and bonds actually outperformed target date funds using a Monte Carlo simulation with data from 1871 to 2011. What’s even more interesting is that a target date fund would outperform if it’s reversed, meaning that instead of an initial overweight position in equities in the early years of the fund, a reverse target date fund would be overweight in bonds and gradually start shifting to equities when it approaches the target date. From a risk perspective, target date funds are actually more risky than balanced portfolios especially for young investors! Let’s first start with the risks.

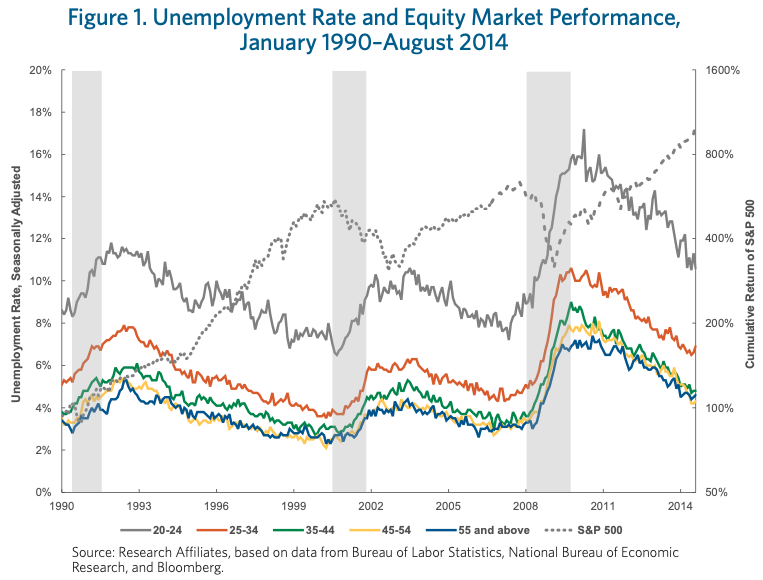

If you’re having a tough time with your personal finances and you’re a young investor, we don’t blame you. A study conducted by Research Associates in 2014 found that young adults’ unemployment rate is more correlated to equity market performance than adults older than 34. This means that if there is a stock market crash, a younger person aged less than 35 is more likely to be unemployed than someone older than 34. Additionally a Fidelity study conducted in 2014 found that of 12.5 million direct contribution (DC) participants, 41% of those between the ages of 20 and 39 withdrew part or all of their DC assets. Combined with the fact that a lot of younger people don’t have savings and are more likely to be unemployed in a bear market, the circumstances could deliver a triple whammy. If their 401k is their only savings:

- They may have to cash out to pay for basic living expenses

- Assets may be less than the amount of money set aside from their paycheck

- They may have to incur a significant penalty from the IRS for early withdrawals

Yikes! Considering that a traditional target date fund is heavily overweight toward equities in the early years of the fund, this could exacerbate losses. If you happen to be one of these people without savings, a target date fund could be your final undoing in a serious bear market. Now let’s look into the numbers to quantify this risk.

To briefly sum up the results of the study in terms of numbers, a target date fund would perform 10% worse than a static balanced 50-50 portfolio of stocks and bonds. As mentioned above, one would have to question why an investor would take on more risk in a target date fund while receiving lower returns, not to mention the expensive fees! If one is comfortable with the same risk as a traditional target date fund, a reverse target date fund mentioned above would actually perform a whopping 22.2% better than a traditional target date fund!

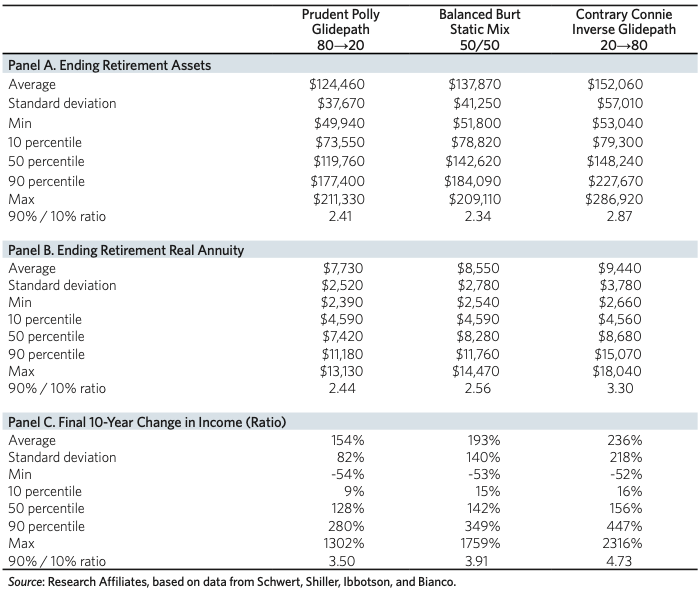

Digging deeper, let’s put this in actual dollar amounts instead of percentages. Assuming that you save $1,000 a year for 41 years toward your retirement, a target date fund would net $124,460 with an 80 to 20 glidepath (80% equities to 20% equities at the target date). However, a static balanced portfolio, 50-50 split between stocks and bonds, would net $137,870 in the same time period, a $13,410 difference! If you’re comfortable with the same risk as a traditional target date fund, a reverse target date fund with a 20 to 80 glidepath (20% equities to 80% equities at the target date) would outperform both netting $152,060, a whopping $27,600 difference from a traditional target date fund! That would be an additional 30k to do whatever you want with it!

Conclusion

Based on the facts and results above, we cannot in good faith recommend a target date fund for an investor seeking good returns. If you want the ease and simplicity of a traditional target date fund, consider buying a balanced index fund or a S&P 500 index fund if for whatever reason you have an aversion to bonds from any of the large asset managers (we will compare these asset managers in a later article. Stay tuned!). However, I personally still advocate for a diverse balanced portfolio as 100% equity exposure is too risky for me and actually performs worse. For those who are more financially savvy and don’t mind getting their hands dirty, we suggest building your own reverse target date fund using index funds or ETFs, depending on your preference such as frequency of trading as index funds only allow you to buy and sell once a day compared to ETFs. We will post another article on building your own reverse target date fund tailored to your needs so stay tuned!

Regardless of what you choose, it’s important to be informed and to consider your risk tolerance and how hands on you want to be in your retirement planning. We know that it can be a long and difficult path but remember that you have us on your journey.

Sources

https://www.researchaffiliates.com/documents/F_2012_Sep_The_Glidepath_Illusion.pdf

Pingback: Beginner’s Guide to Reverse Target Date Funds - Crazy Finances

Pingback: Different Schools of Thought on Investing - Crazy Finances