Summary

Griffon Corporation (“Company”, “Griffon”) is a multinational conglomerate headquartered in New York City. The company conducts its operations through five subsidiaries: The AMES Companies, ClosetMaid, Clopay Building Products, CornellCookson, and Telephonics Corporation. Griffon has been publicly traded since 1961 and is listed on the New York Stock Exchange as a component stock of the S&P SmallCap 600, S&P Composite 1500, and Russell 2000 indices.

Griffon operates as a diversified management and holding company conducting business through wholly owned subsidiaries. Griffon provides direction and assistance to its subsidiaries in connection with acquisition and growth opportunities as well as in connection with divestitures. Griffon focuses on acquiring, owning, and operating businesses in a variety of industries, and intends to continue the growth of its existing segments and diversify further through investments and acquisitions.

Trends

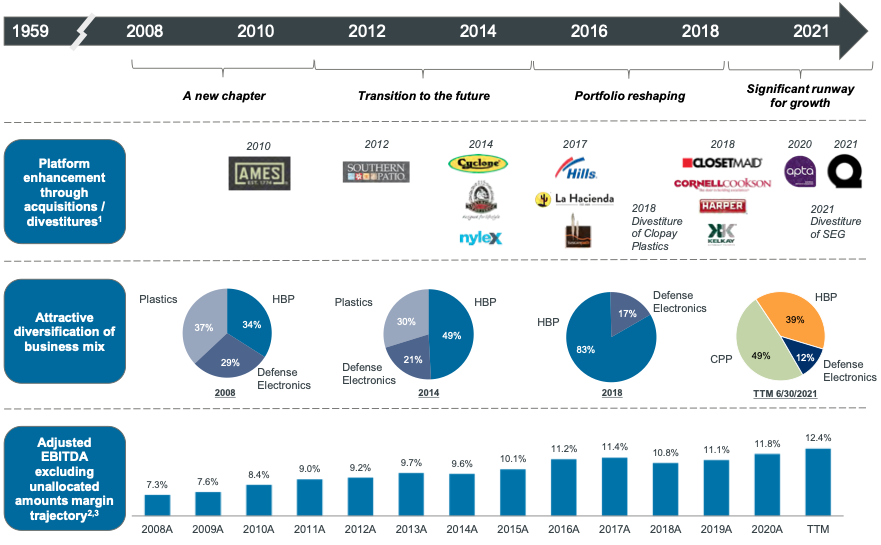

The Company is steadily growing with stable margins. Griffon benefits from increased consumer spending and serves multiple defensive industries. As millennials start raising families of their own and move to suburbs, Griffon is best positioned to benefit from repair, remodeling, and landscaping spend. Growing interest in outdoor living is also driving homeowner investment. Lastly, the U.S. continues to place defense as a top priority including retrofits and upgrades to critical electronics equipment.

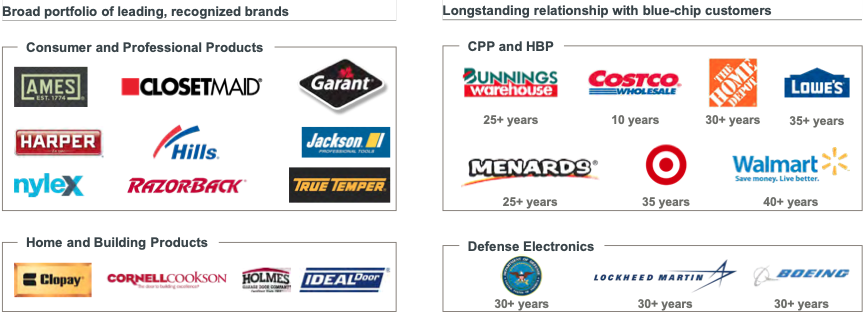

Portfolio and Customer Base

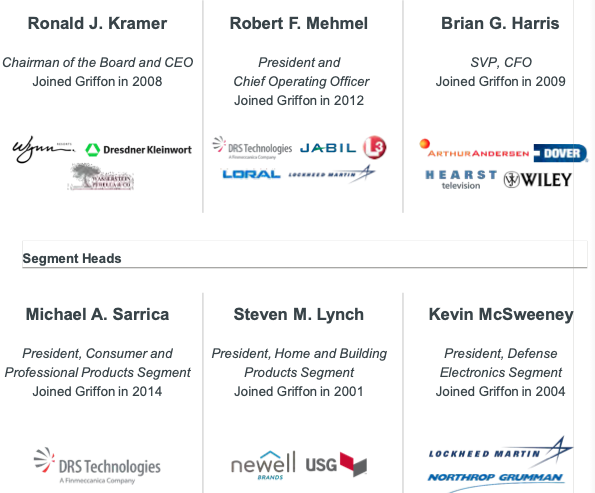

Management Team

The Company’s management team consists of seasoned veterans with backgrounds ranging from Lockheed Martin, Wynn Hotels & Resorts, and Wiley. All have on average of 30+ years of experience with an average tenure of 12+ years at Griffon. They currently have a robust and proactive M&A pipeline to drive further growth and have successfully integrated 12 acquisitions over the last 7 years. Lastly, management is aligned with shareholders with significant insider ownership.

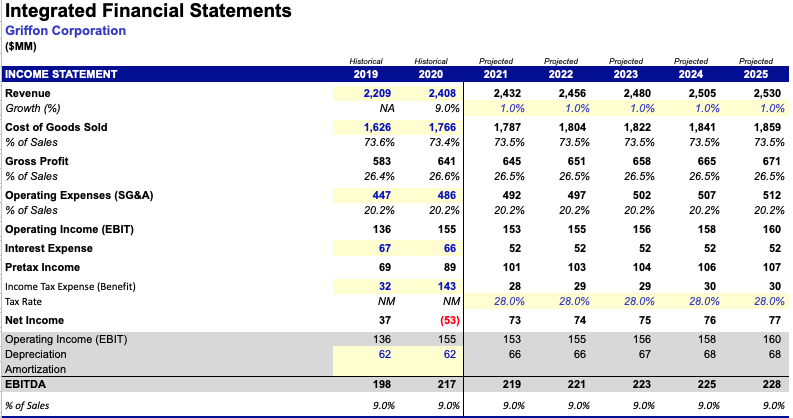

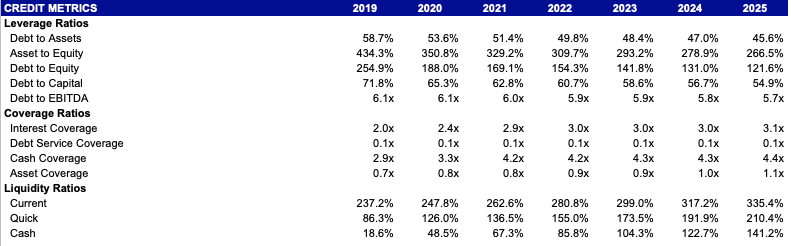

Historical and Projected Financials

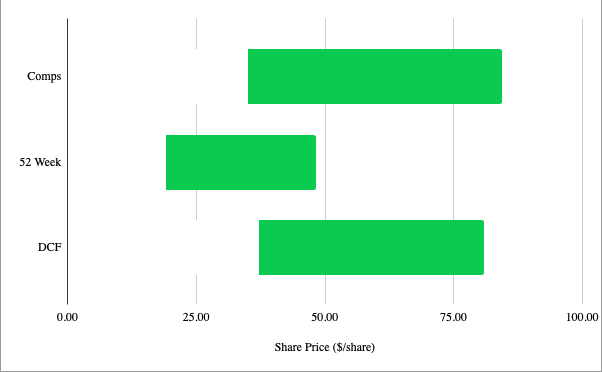

Valuation

Conclusion

CrazyFinances deems a range of $35-42 per share acceptable for the fair value of Griffon with a price target of $40 per share. With the company currently trading at $25.31 as of this article’s publish date, this is a 58% premium to its currently price. Griffon has a solid moat of complimentary and separate product portfolios and there is still opportunity for growth. As long as the company continues to monitor its debt and maintains a robust M&A pipeline, we believe that the company’s true value is $40 per share with a 5 year range.