If you’ve already done your research on leveraged ETFs, you may have seen those articles advocating that holding these ETFs long-term isn’t a good idea. Well, we’re about to prove that myth wrong by looking at some hard data.

So how did this myth propagate? It all started with this formula:

Without getting too much into the weeds, this formula is for volatility drag which is what leveraged ETFs suffer from. Volatility drag states that whenever volatility in the market increases, we lose money from holding the leveraged ETF. The myth is that holding a leveraged ETF (eg. 2x, 3x, etc.) would cause us to lose money with greater leverage when you substitute the variable “x” with the leverage figure in the formula. However, even with a leverage of 1 (aka no leverage), there is still volatility drag according to the formula so basically even with a normal index you’re still technically losing money.

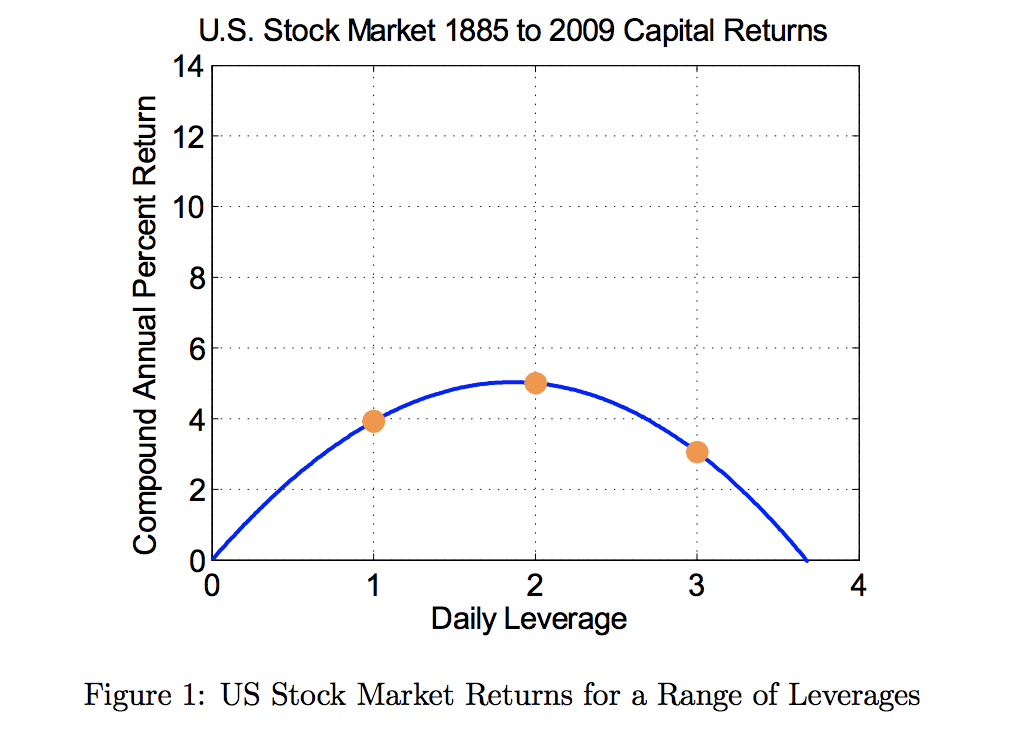

The graph above easily disproves the myth. If we look at returns from the U.S. stock market from 1885 – 2009, we can see that a leverage of 2x beats the compound annual return of a normal or 1x index. Therefore, we can conclude that holding a leveraged ETF long-term actually overcomes volatility drag and can actually beat the index!

So what are the actual downsides of holding a leveraged ETF? Let’s take a look at those below.

High Fees

Leveraged ETFs charge high fees compared to normal indexes, which makes sense because these ETFs are taking on leverage and assembling futures contracts for you. If you are starting with a small account, it wouldn’t make sense because a single futures contract would take up your entire portfolio! Thus, leveraged ETFs are a great substitute but you are paying higher fees for that convenience. These fees eat into your returns.

Tracking Error

While all index funds ultimately suffer from tracking error, big or small, leveraged ETFs tend to have a higher degree of error compared to a normal fund. These tracking errors contribute to the volatility drag which can impact your returns.

Leverage Works Both Ways

Leverage amplifies your returns in a bull market and your losses in a bear market. For example, a 50% drop that a 2x leveraged ETF tracks would result in the fund being wiped out an a 33.4% drop that a 3x leveraged ETF tracks would also result in the fund being wiped out. You can lose all your money in a leveraged ETF.

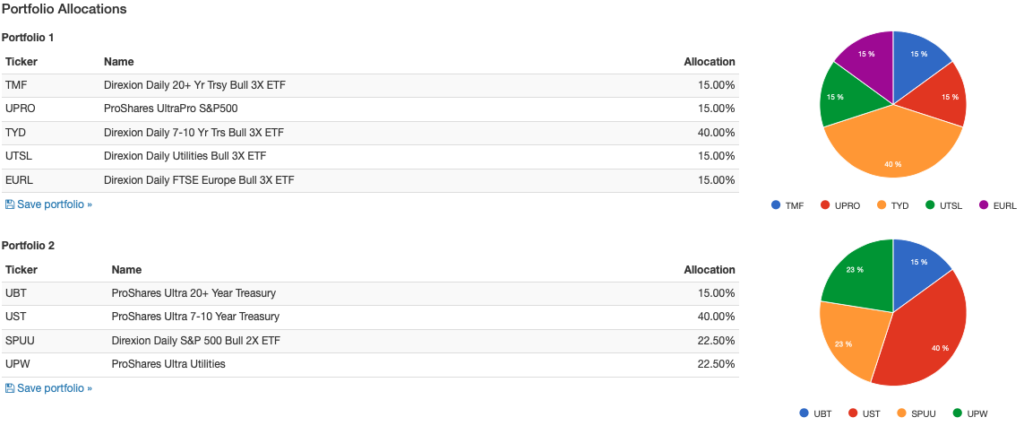

The biggest risk for us as you can tell is the fund being wiped out in a bear market. So how do we mitigate this risk? Fortunately, we all know the wonders of diversification and this is where my boy bonds come in. Let’s take a look at the following allocations below.

Here are the reasons why we chose these indexes for the portfolios.

Treasuries

Both portfolios are 55% weighted toward Treasuries since they act the opposite of stocks. There have been rare moments where both Treasuries and stocks behaved in tandem but for the most part, Treasuries historically have negative correlation with equities. These Treasuries help mitigate the loss should an equity fund be wiped out during a downturn and these bond yields typically drop in a recession resulting in higher prices. This is good for us as a buffer and the leverage amplifies these returns.

S&P 500

The S&P 500 consists of the 500 largest companies in America and are considered to be the most stable compared to the rest of the market. The reason why I selected this over the Nasdaq 100 / QQQ is because the Nasdaq 100 has higher volatility. Remember that we’re trying to not get wiped out in the short term and the chances of that happening are higher when holding leveraged QQQ (the Nasdaq 100 lost 50% of its value during the 2007-2009 crash).

Utilities

Utilities have half the correlation of the U.S. stock market which also serves as a buffer during a crash. Additionally, everyone needs electricity, gas, etc. so holding onto utilities is a good play against a crash.

Europe

I added Europe as a diversification measure in the 1st portfolio as I was unable to find a similar ETF for 2x leverage. Should stagflation in the U.S. occur, the Europe ETF serves as a buffer.

Why no Emerging Markets, Tech, or Commodities?

The reason why we don’t include emerging markets or commodities is because both are volatile which as described above doesn’t bode well for the short-term. Because the volatility on emerging markets is >20% on average compared to the S&P 500 which is <15%, we won’t be including emerging markets to avoid being wiped out. The same also applies to commodities and tech as we don’t want to get 90% wipeout in a short period of time.

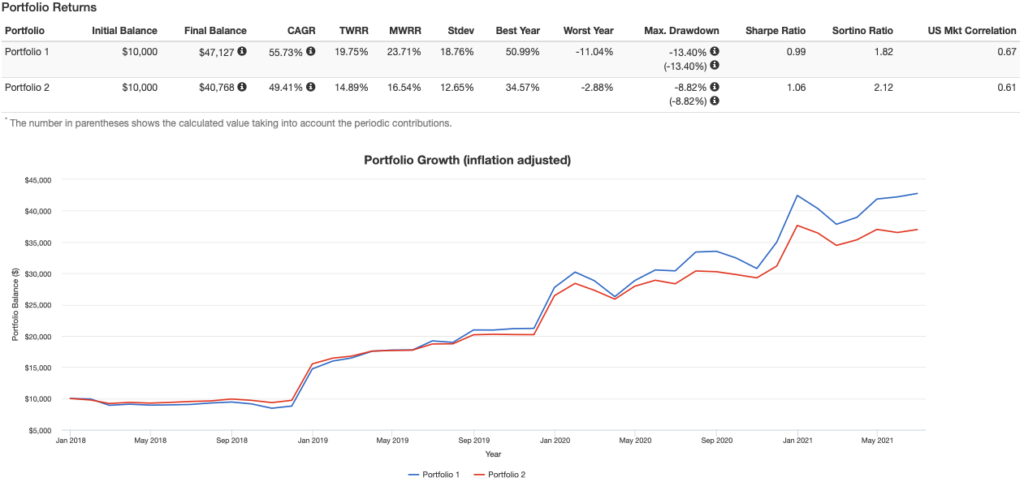

Now let’s look at a backtest of these 2 portfolios.

As you can tell, the 3x portfolio did the best over the time period netting an additional $7k compared to the 2x portfolio. However, the 2x portfolio had a higher Sharpe ratio (which measures return over the risk free rate) and lower max drawdown. It also has a lower U.S. market correlation (0.61 vs. 0.67) but at the cost of lower CAGR by 6%. It is ultimately up to you how much leverage you want but since I can afford the additional risk, a portion of my portfolio utilizes 3x ETFs.

Conclusion

Holding leveraged ETFs long-term is not bad when it comes to volatility drag but there are risks to holding them. We’ve shown that holding a well-diversified asset base of leveraged ETFs mitigate this risk and can be a suitable strategy for those starting with a small account.

Disclaimer

The author holds the 3x ETFs mentioned in this article and is bullish. This article is not investment advice and should be followed at your own risk.