We talk a lot about stocks and companies on this site, but what about real estate? Everyone seems to think real estate is mysterious and its value comes out of thin air but believe it or not, valuing real estate is similar to valuing companies. At the end of the day, when it comes to any investment, stock or real estate, the most important thing we have to look at is free cash flow. In this article we’ll be taking a look at 2 methods of valuation, comparable properties and the income method. Note that this article does not go into what aspects to look for when screening real estate; that will be covered in another article. We’re simply looking at valuation methods for real estate.

Comparable Properties

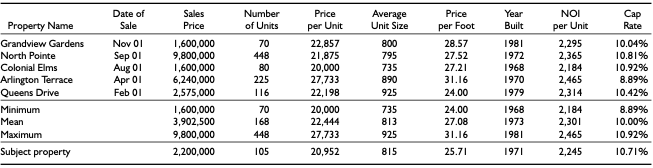

The name is what is suggests. One way to value a property is to search up similar properties and see what they sold at. See below for an example:

These are some of the metrics that we look at such as cap rate, NOI per unit (NOI stands for Net Operating Income which is similar to EBITDA for companies. It is a proxy for free cash flow), etc. Once we assemble a list, we can compare the average of these metrics to the subject property. In the example above, we see that the cap rate of the subject property is 10.71% which is similar to the average cap rates of comparable properties. When we look at the NOI per unit, it’s also similar to the average NOI per unit of the comparable properties. With this valuation method, we can conclude that the subject property is fairly valued compared to similar properties that were sold.

Note that comparable properties valuation mainly applies to properties with 4 units or less. For larger buildings, more emphasis is placed on the income method.

Income Method

The Income Method is an intrinsic valuation of a property. Similar to a DCF or LBO of a company, the income method looks at how much rental revenue the building can generate and arrives to free cash flow. With this information, you can calculate NPV and IRR similar to a DCF of a company. Let’s take a look at an example:

While it may seem like a lot of numbers, it’s actually very simple. Starting from the top, we determine the gross income of the property which mainly consists of rental revenue. One of the value drivers besides improving the property would be the addition of laundry and vending machines, which would fall under other income. Then we determine our operating expenses such as insurance, utilities, taxes etc. to arrive at the NOI. This NOI is used to determine the cap rate which is a common real estate valuation ratio. After calculating the NOI for the projection period, we can calculate the free cash flow after debt service and capex. This is the cash available to the owner.

There are other metrics to consider such as the debt service coverage ratio and cash ROI. For both, a higher number is better. Lenders typically want to see at the minimum of 1.00 for the debt service coverage ratio.

With the income method, we can also calculate our NPV, IRR, and MOIC of different exit years. In the example above, we look at exits in years 1, 3, and 5. As indicated above, an exit in year 1 would result in the highest return when looking at IRR and MOIC. However, it’s important to remember that sometimes it’s not ideal to exit as the market conditions may be for a buyer’s market where property values are depressed or loan covenant restrictions that we must abide to. It’s important to remember that both these methods are simply tools and that we also have to look at factors outside just financial numbers to make a decision.

Additionally, it’s important to remember that the income method is mainly for properties that have greater than 4 units as comparable properties are more rare.

Conclusion

Now you know 2 main methods to value real estate and to make sure that you aren’t being ripped off. Of course, this doesn’t mean that you shouldn’t hire an appraiser because if you plan on getting a mortgage the bank most likely would require you to get one anyway. Additionally, there is no exact property similar to the subject and the income method relies on assumptions. It is equally important to research the market and the property and combining both qualitative and quantitative facts to come to our decision.