This company popped up on my screener as I was looking for undervalued, quality stocks in defensive industries. If you’ve read our previous posts, you’ll find that we currently have a negative value on the market and it is increasingly difficult to find undervalued stocks. I won’t be covering this again as you can go through our past articles. Today we’ll look if B&G Foods (“BGS” or “Company”) is an exception to the market.

Company Summary

B&G Foods is an American holding company for branded foods.[1] It was founded in 1889 to sell pickles, relish and condiments. The B&G name is from the Bloch and Guggenheimer families, sellers of pickles in Manhattan. It is based in Parsippany, New Jersey and has about 2,500 employees.[2] Kenneth G. Romanzi is the company’s CEO and president.[2]B&G has been publicly traded for more than a decade as of 2018 and has been acquiring orphaned brands as part of its growth strategy.[3] Currently, B&G sells frozen and shelf-stable foods.[4]

B&G acquired several brands from Nabisco including Regina Wine Vinegar, Brer Rabbit Molasses, Wright’s Liquid Smoke, and Vermont Maid Pancake Syrup. The company also owns Trappey’s Fine Foods (maker of Trappey’s Hot Sauce from Louisiana and pickled peppers). Other brands include maple syrup and maple candy company Maple Grove Farms of Vermont. From Pillsbury Company, B&G acquired B&M Baked Beans, Ac’cent Flavor Enhancer, Las Palmas Mexican Sauces, Joan of Arc canned ingredient beans, and Underwood meat spreads.[5]

Financial Performance

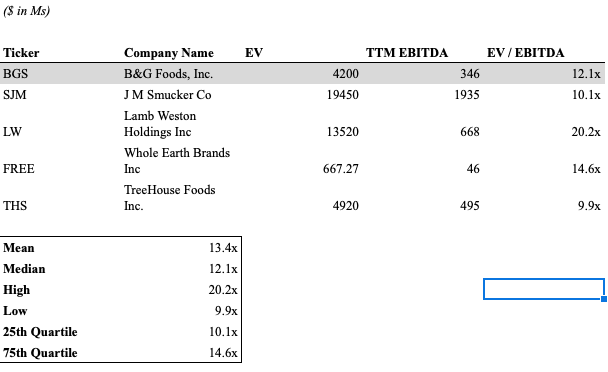

Peer Analysis

Moat

The Company has a diverse brand portfolio spanning from seasoning and syrup products to household offerings. Additionally, despite inflationary pressure the Company has been able to maintain its margins as shown above in the Financial Performance section (P&L statement). Despite supply chain challenges especially for its Green Giant canned products during Q1 2021, the Company has been able to maintain its operations and meet customer needs. The Company’s operational expertise, competent management, and strong brand portfolio are strong tailwinds despite future challenges.

Returns Analysis

Risks

- Company currently has ~$2.4B of debt and is most likely going to take out more debt for acquisitions

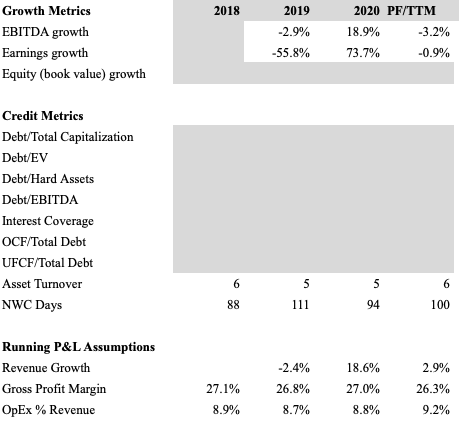

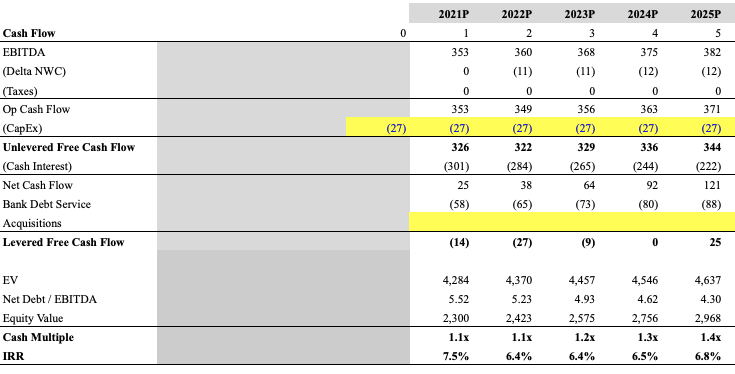

- Based on conservative revenue growth assumptions of 2% per annum with stable margins, the Company will face a liquidity crunch as shown above unless they are able to take out a revolver. This may be more difficult if the Fed does decide to increase interest rates to combat an inflationary environment

- Rising commodity costs and supply chain / procurement challenges may severely impact operations, requiring the Company to maintain its strict cost control

Conclusion

Based on the analysis above, we’ve concluded that BGS is currently a SELL. While we do like management and its brand portfolio, the Company currently has too much debt and its dividend yield is over 6%. We do not think this is sustainable and the Company will either have to spin-off brands in the worst-case scenario to delever or cut its dividend; both will severely impact its stock price. While long-term the Company may be able to succeed, management will need to address the Company’s current capitalization.