Bitcoin, SPACs, Tesla… There’s so much hype in the current market and stocks seem to just keep going up. But, what if we told you, there was an under the radar company that doesn’t even do much with technology that you should add to you your portfolio.

Let me introduce you to General Mills (Ticker: GIS). This giant has been around 1866; that’s 150+ years ago. They make many of the products that you love such as Cheerios, Yoplait, Häagen-Dazs (outside of US & Canada due to licensing agreements), and Lucky Charms to name a few.

This company has a strong dividend and we believe that it could also do well during periods of inflation. It currently pays out a 3.3% dividend and has a PE ratio of 15.45 at the time of this articles writing. With the consumer staples average PE in the low 20s currently, we see General Mills as a solid value play. Add on the dividend, and during periods of low growth, you can still get earnings into your pocket.

With the current fear of inflation hovering and large consumer good manufacturers like General Mills and Kellogg signaling that they are seeing a rise in commodities such as corn and wheat, you may be wondering isn’t that bad for these companies? While raw material price increases are bad for a company’s bottom line (margin shrinks), companies like General Mills will pass the cost to consumers. What will happen is grocery items like Cheerios, Yoplait and others will increase in price to basically adjust for inflation. The consumers then take the brunt of the cost so General Mills can maintain a healthy margin because they know they can’t take a loss on the goods they sell. We can also see from their extensive portfolio that many of the brands they own are in common household grocery lists such as cereal and yogurt. With such a diversified portfolio of brands, the company should be able to stay competitive in the competitive food producer space even after the coronavirus pandemic has subsided.

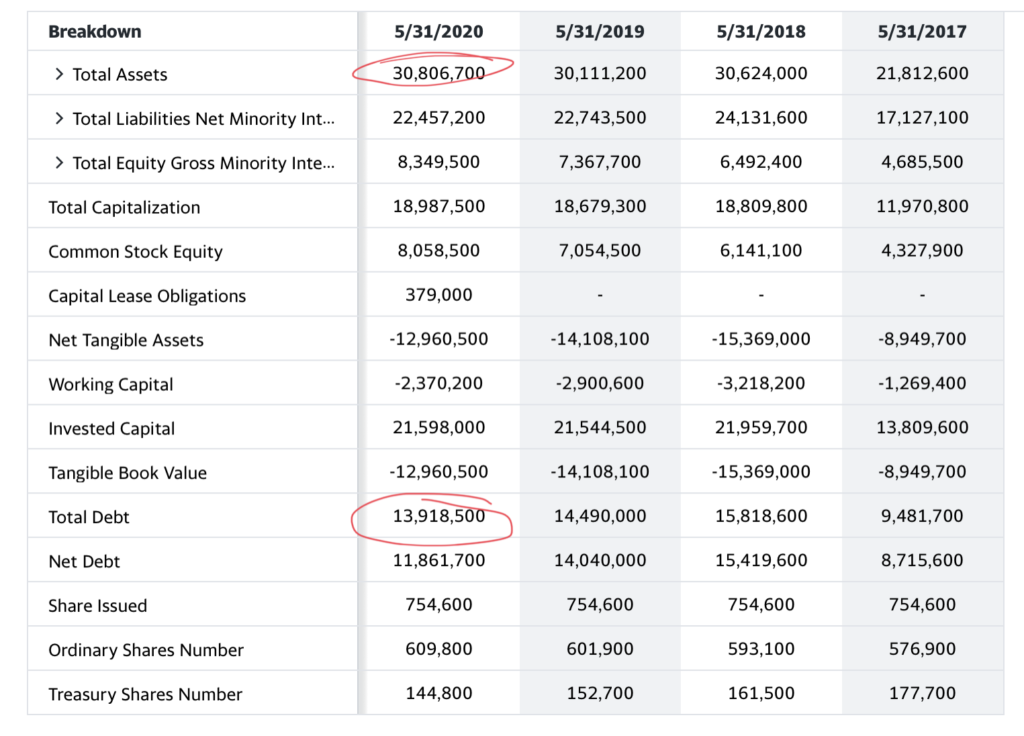

But, some of you may be looking at the balance sheet and wondering, what about all the debt? That’s a good question and General Mills does have quite a bit of debt. Their current debt to asset ratio is .45 which is in line with other similar companies like Kellogg so that’s good. They do seem to be running a bit low on capital which could be a concern when interest rates rise and they have debt they need to start paying. But, with the current fed chair choosing to keep rates near 0 for the foreseeable future, this should not be a huge concern. Hopefully General Mills continues their trend in lowering liabilities to build a stronger balance sheet. Additionally, their earnings have shown continuous year over year revenue growth which is good to see.

So fundamentally they are looking fairly strong. Additionally, their technicals are starting to gain momentum. The 20 day simple moving average is above the 200 day moving average and the 50 day is about to cross over as well which show further bullish momentum.

So yay or nay to General Mills? This is a big yay in our opinion. With a strong portfolio of brands and consistent dividend payouts, General Mills is an equity that can be held on to for decades like Coca Cola.