About to head to college and wondering if you should take out student loans? Continue reading on.

Student Loans

Boy this is my favorite loan. God bless America, while government-backed student loans were initially created with good intentions to support returning veterans of World War II they have now become a colossal mess and thus emphasizing that “the road to hell is paved with good intentions.” What’s better than attending college with large amounts of debt to end up getting a piece of paper with dubious worth? Now I understand why so many in our generation are socialists/communists. All jokes aside, student loans currently consist of $1.6 trillion and many consider it a crisis as a significant portion of graduates are unable to pay their loans back. Fortunately, I am on track to pay off my loans within a year but not many have this opportunity. Many believe that student loan forgiveness is the way to go but here’s why I believe that student loan forgiveness is the wrong approach when it comes to relieving the crisis.

It would increase inflation.

Think about it; where would the money for student loan forgiveness come from? It’s definitely not going to come from taxes as our economy is being hit despite the stock market not reflecting this phenomenon in large part thanks to low interest rates set by the Federal Reserve. We’ve currently seen large increases in M2 supply and any further relief in this economy will only come from monetary policy instead of increases in taxes. If you’re investing in today’s market, the real inflation rate to beat is 9% which means if you’re getting below that number you’re actually losing money.

You may be asking so how do we solve this student loan crisis? Personal opinion incoming, but I believe the best way to solve this crisis is to completely abolish the federal student loan program. Stop the government and its Department of “Education” from interfering with free markets and let the prices decrease. The reason why college tuition continues to increase is because the government essentially subsidizes education through federal student loans. Low interest rates on these loans entice people to take on debt and federal protections tempt those to take large amounts of debt. We have also seen something similar with the housing crisis in 2007 where lax lending requirements essentially propped up increasing home prices and lenders lent money to borrowers with questionable financial characteristics. In the student loan scenario, college tuition prices are being propped up by the government instead of private lenders. Once the government stops subsidizing this industry, we’ll see a drop in college tuition with private lenders becoming more stringent on who they lend to. This in turn will drop the default rates as private lenders seek to lend to students taking on lucrative majors.

The numbers Mason!

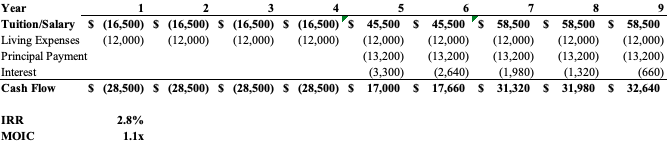

Let’s look at the numbers and determine if it’s worth taking out student loans. Let’s say you attend an out-of-state college for a degree in finance where tuition is $33,000 a year (this is a made up tuition number since we don’t want to get doxx’ed on what college we went to but this is a ballpark tuition for OOS schools not including books and living expenses). We’re assuming that your parents are going to pay half of tuition while the rest will be funded by student loans which translates to $25,000 a year coming from parents. Across a four year period, the total cost of attendance will be $200,000 with $100,000 being our “equity” contribution (I know it’s wrong to compare people to companies but this is a finance blog and there are a lot of similarities between corporate and personal finance).

Out of college, you get an entry-level job as an analyst that pays $70,000 a year. To keep things simple, let’s assume a tax rate of 35% flat across all salary grades. That means your after-tax salary would be $45,500. Then after two years, you get promoted and make $90,000 on a pre-tax basis. Since I’m an Excel guy, let’s look at a spreadsheet.

Business major projected budget:

As you can see across 9 years, we’ve only achieved a 2.8% IRR and a 1.1x cash multiple after taking out $66,000 in loans as the other half was covered by our parents. We were very generous with living expenses assuming that you only spend $1,000 a month including rent and food. We paid off the debt in 5 years. We could theoretically increase the tenor of the loan and pay it off in 10 years to increase our cash multiple but our already low IRR would only continue to decrease due to time value of money.

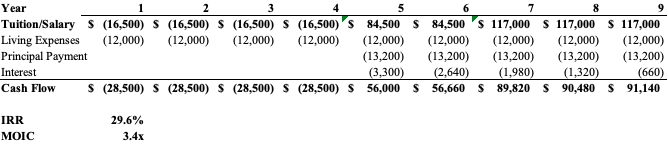

The above was for a business major. Let’s look at a similar forecast for someone who majors in computer science. We’re assuming this person goes to the same school and nothing else changes besides income, which would be $130,000 for the first 2 years with a bump to $180,000 in the 3rd year onwards from a promotion.

Computer science major projected budget:

As you can see, we’re making a healthy amount of income in this scenario and assuming that we continue to live on a student’s budget for 5 years after graduation, we can make a healthy return. We haven’t considered retirement contributions but deduct $25,000 from the cash flow figure of each year ($6,000 towards Roth IRA and $19,000 towards 401k). Keep in mind that with these government-backed retirement accounts, you can only withdraw from your 401k without penalty at age 55 and 59.5 from your IRA. Thus, if you’re planning to retire earlier and are on a FIRE route, you may have to replan your retirement or take the tax penalty on an earlier withdrawal. We’ll cover this in another episode.

Conclusion

To conclude, student loans are a complete sham. Even if you got the cheapest federal loans at a 5% rate, your rate of return is screwed. Keep in mind that student loans may also hinder your future life plans such as buying a home, starting or buying a business, etc. This emotional cost is simply difficult to measure. Only take out loans if you’re planning to study a lucrative major and ideally one that doesn’t require graduate studies (this eliminates biology, chemistry, etc. in the STEM field) and avoid private loans at all costs by going to a community college. Keep in mind that all STEM majors are not equal so do your own research and figure out which one has the best prospects.