We were dead wrong believing people wanted made in the USA, and it cost us millions. People wanted the lowest price.

Mamun Rashid, COO of Auxin Solar which was started in 2008 and has been wrecked by China’s low cost production and economies of scale.

Company Overview

First Solar, Inc (“Company” or “First Solar”) is a provider of photovoltaic (PV) solar energy solutions. The Company designs, manufactures and sells PV solar modules with a thin-film semiconductor technology. The Company also develops, designs, constructs and sells PV solar power systems that primarily use the modules it manufactures and provide operations and maintenance (O&M) services to system owners. It operates through two segments: modules and systems. The modules segment is involved in the design, manufacture, and sale of CdTe solar modules, which convert sunlight into electricity. The systems segment provides power plant solutions in certain markets, which include project development, engineering, procurement, and construction (EPC) services, and O&M services. Its customers include utilities, independent power producers, commercial and industrial companies, and other system owners.

Valuation

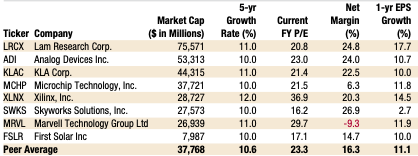

Using the FY2020 diluted EPS of $3.77 and comparable companies above, we’ve come to the following valuation targets:

- Mean: $87.84

- Low: $61.07

- High: $139.11

Risks

- US solar tariff policy remains a wildcard

- Section 201 tariffs if applied would result in $0.025/W decrease in margin and lower valuation by ~$9/share. Currently, First Solar is exempt from these tariffs.

- Increasing competition from Chinese competitors such as JinkoSolar (NYSE: JKS), which is the largest solar panel manufacturer in the world. In totality, China controls 80% of global solar cell manufacturing

- Potential procurement risks of vital components

- China controls 64% of polysilicon material supply worldwide

- China controls 100% of solar ingots and wafers supply

Conclusion

While fundamentally, First Solar does well industry pressure is significant. The Chinese currently dominate the solar cell manufacturing industry and have a sustainable moat due to its procurement advantages, economies of scale, and cost leadership. Customers of these manufacturers primarily care about cost of the product and China has a large moat to reap benefits from this trend. US solar cell manufacturing is unable to sustainably continue competing against the Chinese while Chinese quality only continues to improve. Thus, I’m issuing a Sell rating on First Solar with a price target of $61.07.

Disclaimer

The author currently does not hold any positions in First Solar and does not plan to initiate a position in the next 72 hours.